-

About Us

CMMI Level 5 Certified

Where You Deserve the Positive Outcomes!

Positivity, Purpose, and Perseverance are what make the Protonshub the most sought-after and a leading name in Custom Software Development across the globe. We specialize in Advisory Services, Application Development & Maintenance, Business Process Outsourcing, Enterprise Consulting, End-to-End Technology Services, and Digital Strategy to help make the business world exceptional.

-

Services

Speak with an expert today!

We’d love to resolve your queries with personalized assistance.

Let’s Connect -

Solution

- Industry

- Resources

Aug 29, 2025

Real-World Applications of AI and Blockchain in EnterprisesExplore how AI and blockchain drive innovation in enterprises—enhancing fraud detection, supply chains, healthcare, and cybersecurity.

Read More.png)

Aug 05, 2025

How a Generative AI Development Company Can Help You Build Smarter ProductsDiscover how a Generative AI development company helps build intelligent, scalable products with chatbot development services, automation, and analytics.

Read More

Jul 15, 2025

Chatbot Development Services: What You Need to KnowExplore chatbot development services, types, benefits, and use cases. Learn how custom bots improve engagement, cut costs, and boost efficiency.

Read More

Jul 03, 2025

Understanding Blockchain Development: The Future Backbone of Business TechThis blog explores blockchain development, its key features, business benefits, real-world use cases, challenges, and how to implement it effectively.

Read More.png)

Jun 23, 2025

Enterprise AI Development: A Guide for Business DevelopersExplore how enterprise AI is transforming businesses with key tech stacks, use cases, and strategic insights for business developers and decision-makers.

Read More

Feb 20, 2025

HIPAA Compliant App Development: A Detailed Guide for 2025Learn key steps for HIPAA-compliant app development to ensure secure healthcare solutions. Discover best practices for data security and compliance.

Read More

Feb 18, 2025

How to Create Medical Billing SoftwareGet a step-by-step guide to developing medical billing software. Learn key features, cost, and required tech stack for the development process.

Read More

Feb 12, 2025

How to Make an App like AstrotalkWant to create an astrology app like AstroTalk? Learn about key features, development costs, future trends, development process, and more.

Read More.png)

Feb 05, 2025

How Biometrics Make Payments Easy and SafeLearn how biometrics are changing payment systems by offering a safer and convenient way to complete transactions. Contact us for more information.

Read More

Jan 31, 2025

14 E-commerce Customer Retention Strategies That WorkIs your e-commerce business struggling with customer retention? Try these 14 effective strategies that can transform your approach!

Read More

Jan 27, 2025

11 Essential Features Every Successful E-commerce Website Must HaveIncrease your e-commerce potential. Learn about the 11 crucial features that every successful online store should include for optimal performance.

Read More

Jan 24, 2025

Healthcare CRM: What You Need to Know About Costs, Features, and BenefitsAre you curious to learn about Healthcare CRM? If yes, read this blog to know the costs, features, and more that can help your healthcare practice grow.

Read More

Jan 21, 2025

AI in Energy Management Systems: Driving Operational EfficiencyRead this blog to learn how AI technologies are optimizing energy management systems to improve operational efficiency and cut costs.

Read More

Jan 18, 2025

Your Guide to Designing a Renewable Energy WebsiteLearn how to create an effective renewable energy website with easy tips on design, content, and user engagement.

Read More

Jan 14, 2025

Website Migration Guide: Pre and Post-ChecklistGet ready for a seamless website migration. Follow our pre and post-checklist to ensure everything runs smoothly before and after the move.

Read More

Jan 09, 2025

Application Management Services: A Simple GuideLearn the basics of Application Management Services and how they can improve your IT processes. A simple guide for better application management.

Read More

Jan 06, 2025

Guide to EHR Systems: Features, Benefits, and PricingDiscover everything you need to know about EHR systems. This guide covers key features, benefits for healthcare providers, and pricing options.

Read More

Jan 01, 2025

How to Build a DeFi App in 2025: A Complete GuideReady to create a DeFi app? Our complete guide for 2025 covers everything from key features, development steps, and challenges to help you create a successful DeFi app.

Read More.jpg)

Dec 25, 2024

How to Set Up an Effective Dropshipping Business on Shopify in 2025Ready to start your dropshipping journey? This guide covers everything you need to know about launching a profitable dropshipping Shopify store.

Read More

Dec 18, 2024

Why You Should Hire a Dedicated Remote Developer in 2025Explore the top 9 reasons to hire dedicated remote developers in 2025, from cost savings to niche expertise and clear communication.

Read More

Dec 11, 2024

End-to-End E-commerce Solutions: Why It’s Crucial for Your Business GrowthRead this blog to find out why complete e-commerce solutions are important for your business growth and how they can help you improve your operations.

Read More

Dec 04, 2024

Choosing the Right Technology Stack for Your E-commerce BusinessWant to build a successful e-commerce site? This blog will help you understand how to choose the perfect tech stack for your business!

Read More

Nov 28, 2024

Step-by-Step Guide to Developing a Multiplayer Poker App Like A3 PokerLearn how to develop a multiplayer poker app like A3 Poker with our easy step-by-step guide. Build your app today and engage players worldwide!

Read More

Nov 21, 2024

How to Develop an App Like UEFA GamingLearn how to build an app similar to UEFA Gaming! Discover essential tips and tricks to bring your gaming ideas to life. Contact us to know more.

Read More

Nov 13, 2024

The Role of AI in Quick Commerce App Development for Personalized User ExperienceLearn how AI is transforming Q-commerce app development to create a more personalized shopping experience for users. Contact us to know more.

Read More

Nov 06, 2024

Why Quick Commerce App Development is Essential for Retail Businesses TodayThinking about app development? Find out how Q-commerce can transform your retail business by speeding up deliveries. Contact us for more details.

Read More

Oct 30, 2024

Top Features to Include in a Quick Commerce App for Maximum User EngagementFind out the best features to include in your quick commerce app. Make shopping fun and keep users coming back for more! Contact us for more details.

Read More

Oct 24, 2024

How to Build an App Like GrabReady to build a unique food delivery app? Learn how to create a Grab-like app with essential features and expert services. Contact us today.

Read More

Oct 17, 2024

Chatbot vs. Live Support: Which Is Better for Your Business?Explore the differences between chatbots and live support to determine which solution best fits your business needs. Discover the pros, cons, and more.

Read More

Oct 10, 2024

Why Every Business Needs a Custom Chatbot: A Comprehensive GuideBoost your business with a custom chatbot designed for your unique needs. Explore the benefits that drive customer satisfaction and growth.

Read More

Oct 03, 2024

How to Develop an App Like GEICODiscover essential steps and features to develop a successful insurance app like GEICO. Learn about user experience and innovative functionalities.

Read More.jpg)

Sep 26, 2024

Top 10 Use Cases of AI-Powered Chatbots in HealthcareLearn about the top 10 use cases of AI chatbots that enhance patient satisfaction, reduce wait times, and optimize healthcare services.

Read More

Sep 19, 2024

How Custom Chatbots are Revolutionizing Patient Care in the Healthcare IndustryUncover the power of custom chatbots in healthcare. From appointment scheduling to symptom assessment, see how they enhance patient experiences and care.

Read More

Sep 13, 2024

How to Develop a Food Delivery App Like ZeptoUncover the secrets to building a successful grocery delivery app like Zepto, including must-have features and steps for quick commerce.

Read More

Sep 09, 2024

How to Develop a Food Delivery App Like SkipTheDishesDiscover the essential steps to develop a food delivery app like SkipTheDishes. Learn about key features and steps to ensure your app stands out.

Read More

Sep 03, 2024

Building a WordPress E-commerce Store: A Complete GuideTransform your WordPress site into a thriving e-commerce store! Follow our complete guide for expert tips on setup, customization, and boosting sales.

Read More

Aug 30, 2024

How to Optimize WordPress Website for Performance and SpeedIs your WordPress site slow? Find out how to optimize performance and speed with our comprehensive guide on best practices and tips.

Read More

Aug 26, 2024

How to Develop a Mobile App Like ZalandoDiscover how to develop a successful mobile app like Zalando. Learn essential strategies, features, and steps to bring your fashion app idea to life!

Read More.jpg)

Aug 19, 2024

Shopify vs. WooCommerce: Which Platform is Right for Your Business?Explore the pros and cons of Shopify and WooCommerce. Make an informed decision to elevate your e-commerce strategy and maximize profits.

Read More.jpg)

Aug 12, 2024

How to Set Up Your Shopify Store: A Step-by-Step GuideReady to start your online business? This guide walks you through every step of setting up your Shopify store, from design to launch. Start selling today!

Read More

Aug 06, 2024

Optimizing Your Shopify Store for SEO: Best PracticesElevate your Shopify store's search engine rankings with these SEO best practices. Discover tips on canonical tags, site speed, and more to drive traffic.

Read More.jpg)

Jul 31, 2024

How to Build an NFT Marketplace Like OpenSeaLearn how to create an NFT marketplace similar to OpenSea. Discover essential features, technologies, and strategies to launch your platform successfully.

Read More

Jul 26, 2024

How to Build a Hotel Booking App Like OYOWant to build a hotel booking app like OYO? This guide covers everything from market overview and features to strategies for a successful app.

Read More.png)

Jul 23, 2024

How to Build a Restaurant Booking App Like OpenTableLearn how to create an OpenTable clone app that streamlines reservations and dining experiences. Discover key features, strategies, and more.

Read More

Jul 16, 2024

How to Build an App Like NetmedsUnlock the secrets to developing a Netmeds clone app. Explore the must-have features, costs, market stats, revenue models, and more.

Read More

Jul 12, 2024

How to Build an App Like SheinWhether you're a startup or an established business, our guide will walk you through the process of creating an e-commerce app similar to Shein.

Read More

Jul 08, 2024

Blockchain Development Guide: Everything You Need to Know in 2024Explore the latest trends shaping blockchain development in 2024. This guide covers everything you need to know to stay ahead in this evolving field.

Read More

Jul 03, 2024

How Blockchain Technology Can Revolutionize the Fintech IndustryGet ready to discover how blockchain is transforming the fintech industry by increasing security, reducing costs, and enabling faster transactions.

Read More

Jun 28, 2024

Understanding Generative AI: Can it Create the Next Killer Mobile App?Dive into the world of generative AI and discover how it can be leveraged to create innovative, user-centric mobile apps that redefine the industry.

Read More

Jun 24, 2024

Leveraging AI and Machine Learning for Enhanced Stock Insights in Your AppLearn the right way to harness the power of AI and ML to transform your app's stock analysis features, providing users with a competitive edge.

Read More

Jun 19, 2024

Real-Time Data Integration: Challenges and Solutions for Stock Market AppsLearn how to overcome data integration challenges in stock market apps by using real-time data integration solutions for a better user experience.

Read More

Jun 14, 2024

How to Build a Crypto Exchange Platform Like BinanceDevelop a crypto exchange platform similar to Binance with this detailed guide. Learn about the key features, advanced features, cost, steps, and more.

Read More

Jun 10, 2024

How to Build an App Like RobinhoodFrom key features, steps, and costs to the best monetization strategies, learn everything about building an app like Robinhood.

Read More

Jun 05, 2024

How to Develop a Food Delivery App Like MenulogLearn how to create a food delivery app like Menulog. This guide covers the key features, steps, challenges, and costs of developing a Menulog-clone app.

Read More

Jun 03, 2024

How to Build a Shopping App Like Costco?Are you interested in building a shopping app like Costco? This guide discusses the steps, key features, costs, and more to develop an app like Costco.

Read More

May 29, 2024

Why Hire Dedicated Developers Instead of Freelancers?Unlike freelancers, dedicated developers prefer quality over quantity and increase efficiency. This is not it. Read this blog to learn more about the benefits.

Read More

May 24, 2024

How Much Does It Cost to Hire a Software Developer in India?Want to hire a software developer in India but don’t know how much it will cost? Read this guide to learn everything to make an informed decision.

Read More

May 20, 2024

How to Make an Online Shopping App Like AmazonWant to create an online shopping app like Amazon? Read this guide that covers everything you need to know, from features to best practices.

Read More

May 14, 2024

How to Develop an App Like GrowwAre you planning to develop a stock trading app like Groww? Read this blog where we have discussed everything from steps to monetization strategies.

Read More

May 10, 2024

The Ultimate Guide to Building a Job Portal in 2025Struggling to develop a job portal in 2024? Not anymore! Read this comprehensive guide to gain insights into creating a successful job portal on budget.

Read More

May 07, 2024

How to Develop an App Like DoorDashThis blog discusses the steps involved in creating a successful app like Doordash, from market research to post-launch support. Read now.

Read More

May 03, 2024

How to Build An App Like AirbnbLearn everything about building a robust vocational rental app like Airbnb, from steps and cost to features in this detailed guide.

Read More

Apr 29, 2024

How AI is Transforming Electric Vehicles: Benefits and ChallengesWith AI evolving, you can expect to see these transformations in the EV sector such as smart charging stations, route optimization, and more.

Read More

Apr 25, 2024

AI Coach in Your Pocket: Exploring the Benefits of AI-Powered Fitness AppsDo you want to know the benefits of AI-powered fitness apps or how developers can overcome AI-fitness app development challenges? Read this blog.

Read More

Apr 18, 2024

The Future of Fitness: How AI is Revolutionizing Workout AppsRead this blog to learn how to build a fitness app, the compliance involved in building fitness apps, the cost to build a fitness app, and more.

Read More

Apr 15, 2024

How to Make an App Like Snapchat: Expert Guide and Tips [2024]On average, the cost varies between $40,000 and $300,000. But factors like the app’s complexity, UI/UX design, and more affect the cost.

Read More

Apr 12, 2024

How to Build AI-Powered Apps in 2024: A Step-By-Step GuideFollow these 6 steps to successfully build AI-powered apps. Also, check the cost of development and use cases of AI-powered apps.

Read More.jpg)

Apr 10, 2024

Chatbots in E-commerce: Benefits + Use Cases ExplainedRead this blog to understand the basics of chatbots in e-commerce, their benefits, challenges during integration, use cases, and future trends.

Read More

Apr 08, 2024

Safeguarding Your E-commerce Site: Tips and Strategies for SecurityWe have discussed common attacks on e-commerce websites and essential tips to improve their security. Read the full blog to bulletproof your website.

Read More

Apr 02, 2024

E-commerce Personalization: How to Tailor the Shopping Experience for Every CustomerE-commerce personalization impacts 90% of customers. So, follow these e-commerce personalization strategies for engaging customer experience.

Read More

Mar 26, 2024

The Ultimate Guide to Optimizing Your E-commerce Website for Search EnginesThis ultimate guide discusses ways to optimize e-commerce site through 6 impactful best practices. Follow these tips to have a well-optimized website.

Read More

Mar 19, 2024

Unlocking Efficiency: How Healthcare Mobile App Development Services Are Streamlining OperationsWant to know how healthcare mobile app development services are streamlining operations? Read this detailed blog to gain a complete understanding.

Read More

Mar 14, 2024

Clutch Names Protonshub Technologies as one of the Game-Changing Android App Developers in IndiaProtonshub Technologies is named one of the game-changing Android app developers in India. Do you have a project? Contact us. We’d love to help.

Read More

Mar 12, 2024

Artificial Intelligence in the Healthcare Industry: A Statistical AnalysisAI in healthcare is expected to increase to $187 billion by 2030, suggesting that AI is capable of delivering better outcomes

Read More

Mar 01, 2024

How Much Does It Cost to Build An App [Complete Cost Breakdown]Have you ever heard the phrase “there’s an app for everything”? Well, it’s true!

Read More

Feb 27, 2024

Google Gemini Pro: Everything You Need to Know About This Next-Gen AIGoogle, the tech giant, has made headlines with Gemini Pro, a flagship suite of generative AI models, services, and apps. After releasing Bard as a trailer, Google launched Gemini Pro AI, the most capable and Largest Language Model (LLM). This AI technology is guaranteed to leave a domino effect on all of Google’s products and mobile applications.

Read More

Feb 23, 2024

Salesforce Development Lifecycle: Stats, Process, Models, And BenefitsSalesforce is a growing tool that is swiftly becoming popular in various industries. That’s because it has all the necessary features that a business needs to accelerate its growth. From lead management, and managing & storing customer data to improving, Salesforce can do it all.

Read More.png)

Feb 19, 2024

A Comprehensive Guide to Creating Software GDPR-CompliantWith technology at the forefront, businesses and their possessed assets have been at risk of cyber theft and data breaches.

Read More

Feb 16, 2024

AI in E-commerce: 8 Ways It’s Transforming the BusinessArtificial Intelligence no longer revolves just around scary and futuristic movies; it is making headlines and can be found everywhere. Among the list of industries that are hopping on the trend of adopting AI, e-commerce has been an early adopter in implementing and improving through the power of AI.

Read More

Feb 13, 2024

Top Emerging Web Design Trends for 2024 and Beyond [Updated]With the fresh start of 2024, it's time to look at the top emerging web design trends for this year and beyond.

Read More

Feb 08, 2024

Best Practices For Your Mobile App Security in 2024Did you know that global phone usage has increased to 7.07 billion?

Read More

Feb 05, 2024

AI In Healthcare: Benefits, Applications, and Common ChallengesAI in healthcare has become more effective in helping physicians and other healthcare providers. It not only offers a genuine chance for professional advancement but also makes healthcare services more affordable.

Read More

Jan 30, 2024

Choose the Best Developers To Build Your Dating AppA dating app is an excellent way to socialize and find your love matches. Or can meet your better half through a casual relationship as well.

Read More

Jan 25, 2024

Choosing the Right Tech Stack for E-commerce Mobile Apps in 2024In the ever-changing world of e-commerce, choosing the right technology stack for your e-commerce app can make all the difference.

Read More

Jan 22, 2024

Tech Meets Love: The Coolest Features Coming to Dating Apps in 2024Online dating apps have established themselves as a key player in social connections. As a part of the dramatically changing tech landscape, dating apps are evolving the way people build relationships.

Read More

Jan 19, 2024

Front-End Development in 2024: Next.js vs React for Building Modern Web ApplicationsReact has been the top choice of developers for a long time but then it started demanding something more. That’s when the Next.js entered with its better capabilities.

Read More

Jan 15, 2024

White-Label vs Custom-Built Taxi App: Which One is Better?Did you know the revenue of the taxi booking industry is expected to reach US$165.60bn in 2024?

Read More

Jan 11, 2024

Unlocking Business Potential with Salesforce DevelopmentDid you know that investing in Salesforce development services can greatly benefit businesses?

Read More

Jan 08, 2024

Exploring the Best Back-end Development Trends For 2024Are you feeling the pressure to keep up with the ever-evolving user expectations? If yes, check out the top trends of 2024 that will help you stay relevant in the market.

Read More

Jan 03, 2024

The Role of AI and AR in Modern Salon Booking AppsArtificial intelligence is dominating the business activities of almost all industries, including the beauty salon sector. From appointment scheduling to marketing & promotions, artificial intelligence in the beauty industry is emerging as a new trendsetter in the marketplace.

Read More

Jan 02, 2024

A Comprehensive Guide To User Personas In Modern App DevelopmentIf your product has a good amount of users, it means the product has the potential to become successful! But you also need to figure out what group of people does not resonate with your business or products.

Read More

Dec 28, 2023

Scalability Challenges in MVP Development and How to Overcome ThemMVP app development has always been a smarter choice. But scaling it into a full-fledged product is a complicated process.

Read More

Dec 26, 2023

The Role of Artificial Intelligence in Enhancing OTT Content Recommendation AlgorithmsWith OTT platforms gaining popularity, the way we consume digital content has changed.

Read More

Dec 21, 2023

AR and VR in E-Commerce Apps: Enhancing the Online Shopping ExperienceDid you know that almost 78.65% of shoppers are known to abandon their shopping carts? While the shopping cart abandonment reasons are multiple, there is one sure-shot way to persuade customers to complete a purchase before they leave the website.

Read More

Dec 18, 2023

React UI Libraries for Building Impressive Web ApplicationsDid you know that almost 75% of consumers have admitted to judging the credibility of a website by the way it looks? It means a large part of a website’s success depends on the design and quality of the website.

Read More

Dec 15, 2023

Things to Consider While Choosing a Software Development CompanyThe stakes get high when hiring a software development company because you need to invest a significant amount of resources, capital, and time in the process. Also, with so many companies offering custom software development services, choosing the right vendor becomes difficult.

Read More

Dec 12, 2023

How to Build a Salon Appointment Booking App?Finding the best salon app and booking an appointment can be a daunting task. It can take too much time and energy, and people rarely have time to call a salon to book an appointment. This thing has created a gap in the market.

Read More

Dec 08, 2023

Complete Guide to E-commerce App Development: Cost & FeaturesEver since the 2000s, the eCommerce industry has been on a meteoric rise, with no sign of downfall.

Read More

Dec 05, 2023

9 Reasons Why You Need an E-commerce Mobile App in 2024When was the last time you had purchased something online? A majority of you would say a week or two ago.

Read More

Nov 30, 2023

How Much Does It Cost To Hire App Developers In Florida?Hiring mobile app developers is a challenging task, but not when you know the right process.

Read More

Nov 29, 2023

The Future of E-commerce in 2024 and BeyondA study has revealed that worldwide e-commerce sales have reached $5.7 trillion in 2022 This figure shows an optimistic projection of this industry for the upcoming years.

Read More

Nov 27, 2023

Mobile App Architecture Designing: Your Step-By-Step Guide for 2024The mobile app development market is incorporating new technologies and safety standards for steady growth. These mobile apps offer a better user experience, which has increased our dependency on them, making them a one-stop solution for day-to-day tasks.

Read More

Nov 23, 2023

Scaling Product After Successful MVP Launch: A Complete GuideInvesting in MVPs or Minimum Viable Products is far better than investing in a full-fledged product because it provides clear market validation and audience feedback.

Read More

Nov 20, 2023

Swipe Right On Safety: 9 Things To Consider When Creating Dating AppsThe use of dating apps has increased drastically, causing the market to grow to $8.64 billion. As per research, out of every 10, almost 3 adults are registered on dating apps.

Read More

Nov 14, 2023

How Much Does It Cost to Build a Fantasy Sports App?The World Cup fever is over with the winning strike of the Australian cricket team, but the craze for fantasy sports apps is still there.

Read More

Nov 10, 2023

A Complete Guide to Fantasy Sports App Development in 2024Almost everyone of heard about Dream11 at least once in their life, which is nothing but a fantasy sports app. For all the sports fan out there, apps like Dream11 is an innovative way to connect users with their favorite sports in a more realistic way.

Read More

Nov 07, 2023

The Role of User Feedback in MVP DevelopmentBuilding a successful minimum viable product (MVP) app is an important step in any organization’s development process. The final goal of a minimum viable product is to validate the product idea quickly in the market while also reducing the associated risks with the development process.

Read More

Nov 03, 2023

Impact of Digital Transformation on Enhancing Customer ExperiencesIn today’s soaring dependency on digital platforms, organizations are countering many challenges to deliver exceptional customer experiences. This is where digital transformation opens new doors of opportunities.

Read More

Oct 31, 2023

How to Create a Dating App at Low Cost?Are you considering developing a dating app but concerned about the price?

Read More

Oct 30, 2023

Choosing the Right Tech Stack for Your MVP: Best PracticesBusinesses that are willing to grow faster must focus on scaling properly. But how can it be done? The key lies in selecting the right tech stack so you can create a functional and robust MVP.

Read More

Oct 27, 2023

10 Things to Consider While Developing a Mobile AppWith more people relying on mobile apps for day-to-day tasks, this industry is booming with no signs of slowing down. A report by Statista has estimated that the number of mobile app downloads is going to cross

Read More

Oct 24, 2023

Unlock the Success: Top 10 Benefits of Hiring Dedicated DevelopersWith the increase in globalization, outsourcing dedicated developers have become a popular and cost-effective solution.

Read More

Oct 19, 2023

Collaborating with App Developers: A Guide for Non-Technical Startup FoundersDid you know that 15.4% of the US population is involved in startups yet the rate of failure for the same is considerably high? But why does it happen? It happens due to lack of funds and high product demand.

Read More

Oct 17, 2023

Guide to Building an On-Demand Courier Delivery ApplicationThe on-demand apps have changed the user experience in a positive way. Among these, the courier delivery apps have greatly contributed to the customer’s rising demands.

Read More

Oct 13, 2023

How to Develop a Logistics App like PorterDid you know that online transportation services have developed into a leading industry that holds the power to pique the public’s interest? In the year 2022, the global transportation market was valued at

Read More

Oct 11, 2023

How to Develop Travel App - Features, Cost & Technology StackDid you know that the digitalization of the travel industry has changed many traditional processes? For instance, now people use travel apps to make reservations, buy tickets, choose destinations, and get around. The trip planning has become much easier and quicker.

Read More

Oct 09, 2023

Important Things to Consider in Software Development [Full Guide]Do you know what makes or breaks a successful software development? It’s the lack of strategic planning.

Read More

Oct 06, 2023

Effective UI/UX Strategies for E-commerce App SuccessOne of the biggest challenges for e-commerce businesses is how to convert visitors into customers. By providing relevant products and services, you can make more people visit your website. But there’s more to the story.

Read More

Oct 02, 2023

Prototype vs. MVP: Which One Do You Need?Businesses of any size willing to develop a successful product can use the technique of prototype or MVP. While using one of these techniques, companies should get feedback from their targeted customers to improve their position in the market and reduce costs.

Read More

Sep 29, 2023

6 Ways Python Development Can Benefit Your BusinessIn recent years, Python has become one of the most recognizable programming languages worldwide. It is being used in everything from building websites and software testing to machine learning.

Read More

Sep 25, 2023

Challenges and Solutions in Travel App DevelopmentTraveling is not just a luxury, it has become a hobby for many people. That’s because when we travel, meet new people, learn new things, and click memorable pictures. Also, it has emerged as a new source of income.

Read More

Sep 21, 2023

How to Track Content Marketing KPI in B2B MarketingCompanies around the globe are spending almost one-third of their budget on content production and distribution.

Read More

Sep 18, 2023

How to Develop a Doctor’s Appointment Booking App (Step-by-Step Guide)Believe it or not, we are heavily dependent on applications to complete our day-to-day tasks. Be it taxi booking, grocery, or dating, we need apps to do almost everything.

Read More

Sep 14, 2023

Choosing the Right Technology Stack for Your Taxi Booking AppNone of us have ever thought about getting picked up and dropped off by a taxi without yelling out the directions to the driver. But, with the advent of technology and the emergence of on-demand taxi-booking platforms, all of this has been like smooth sailing on a calm sea.

Read More

Sep 13, 2023

Challenges and Solutions in Healthcare App DevelopmentBy the year 2028, the global healthcare app industry is expected to reach $314.60 billion. It is because, with the rise in demand for digital healthcare, the need for developing health solution apps has also increased.

Read More

Sep 08, 2023

Website Conversion Rate Optimization Strategies in 2023One of the main purposes of a website is to drive conversion. The more people sign up for the products and services, the better will be the revenues.

Read More

Sep 06, 2023

How Much Does It Cost to Develop a Dating App Like Hinge?Fun and interactive dating apps like Hinge have changed the way people meet and date.

Read More

Sep 04, 2023

Boosting Productivity: How Implementing an ERP System Can Streamline Your Operations?If you look back to the time when manually handling operations was the only way to get tasks done seems quite challenging. Now, since technology has significantly emerged, all these tasks can be done in the blink of an eye.

Read More

Aug 30, 2023

Building Scalable Web Applications with ReactJS in 2023With the emergence of new technologies, developing mobile-friendly applications has become a common phenomenon. However, each project demands the use of different technologies.

Read More

Aug 24, 2023

9 Reasons: Why Startups Should Hire Developers on ContractWhether you plan to start a small or large business, the process can be challenging. That’s because you need to conduct detailed market research for your product or service to create a competitive marketing strategy.

Read More

Aug 23, 2023

How Does ERP Help in the Manufacturing Industry?Is your organization keeping up with the ever-changing pace of the manufacturing Industry?

Read More

Aug 21, 2023

How to create a dating app like Tinder?Ever wanted to experience what dating another person feels like but don’t know how? Well, it can be embarrassing to just ask any random guy/girl if they wanna date.

Read More

Aug 18, 2023

11 Common Problems In the Manufacturing Industry That ERP SolvesThe Enterprise Resource Planning (ERP) system in the manufacturing sector has transformed many organizations from their core. This intense growth has only been possible due to ERP’s capacity to unlock better opportunities and efficiency in solving manufacturing issues.

Read More

Aug 17, 2023

The Future of Taxi Booking Apps: Trends and InnovationsWhen was the last time you halted a taxi by waving your hand? Probably you don’t remember and neither do any of us when we did the same because we have gotten into the habit of booking taxis via mobile phones.

Read More

Aug 14, 2023

How to build a stock trading app (Step by step guide)Does the emergence of stock trading applications intrigue you enough to invest in one by yourself?

Read More

Aug 10, 2023

React Hooks Deep Dive: Advanced Usage and Patterns in 2023Among JavaScript developers, React remains the preeminent choice for enhancing user interfaces. Its emphasis on functional programming principles, such as pure functions, props, and state, empowers engineers to craft robust web applications.

Read More

Aug 07, 2023

How Does Your Website’s UI/UX Impact Your Business Growth?Are you tired of dealing with increasing bounce rates, unsatisfied customers, and decreasing website visitors?

Read More

Aug 04, 2023

The Role of Artificial Intelligence in FinTech: Revolutionizing Customer Experience and Risk ManagementArtificial intelligence has molded the way how FinTech Industry works.

Read More

Aug 03, 2023

Benefits Of Hiring an India-Based Ruby on Rails Development CompanyAre you having trouble deciding whether to hire a Ruby on Rails development company from India?

Read More

Jul 31, 2023

Emerging Trends in Artificial Intelligence and Machine Learning: The Future of ITArtificial intelligence (AI) and machine learning (ML) are rapidly transforming the world of information technology (IT).

Read More

Jul 28, 2023

Exploring GraphQL in Ruby on Rails: A New Approach to API DevelopmentThe new age of web development has created enormous opportunities for new software, which needs APIs for seamless communication. The fact isn’t hidden from anyone that APIs (Application Programming Interfaces) are essential to creating modern applications.

Read More

Jul 26, 2023

Exploring React Native Libraries and Tools for 2023 DevelopmentReact is one of the most used javascript libraries among developers who wants to build a scalable and robust mobile application. It will continue to flourish in the coming years, owing to the advancement and innovations.

Read More

Jul 23, 2023

Exploring the Impact of Fintech in Financial Services: Disruption and OpportunitiesRecent years have seen a significant change in the banking sector as new fintech businesses have appeared, offering cutting-edge technologies and services that alter how banks conduct business.

Read More

Jul 21, 2023

The Rise of Telemedicine: Advancements in Healthcare Delivery and AccessibilityEver experienced a situation where you needed immediate medical assistance but had no one near you? Well, this is a common situation in rural areas where good medical service is located far from where you live.

Read More

Jul 14, 2023

Low-Code and No-Code Development: Accelerating Application DeliveryWhen they say choose an IT career, most of them meant programming. But what if I say you don’t need to be a programmer in order to develop a website or an application?

Read More

Jul 13, 2023

How to Build a Mobile App With a Limited Budget?There was a time when only large organizations considered having an app for their business. Now, the times have changed, every company nowadays, despite its size is looking to have an app developed for N number of good reasons.

Read More

Jul 12, 2023

How to Build a Progressive Web App (PWAs) with ReactApps were just a mere idea when it was first introduced decades ago. People didn’t have any idea about how these apps were going to change their lives completely.

Read More

Jul 11, 2023

Leveraging Sales and Marketing Alignment for Revenue GrowthSales and Marketing, both are essential pillars of an organization. The fact that sales department converts the leads to closure, and the marketing department creates brand awareness via advertising, content creation, and social media handling.

Read More

Jul 10, 2023

Unleashing the Power of Personalization: How Automation Can Supercharge Your Sales and Marketing EffortsToday, every customer looks for achieving tailored experiences that meet their needs. Personalization is a significant factor when it comes to sales and marketing.

Read More

Jul 07, 2023

Streamline Your Sales Process with Marketing Automation: A Step-by-Step GuideImagine having tons of work on priority and you are stuck doing chores that can be automated if you would have thought in a more innovative way.

Read More

Jul 03, 2023

The Role of AI in Banking Software DevelopmentPeople have already anticipated the potential of AI, thanks to the tools like ChatGPT, Adobe Firefly, Writesonic, and many more. Artificial Intelligence has all the hype for today and its implementation in the banking industry has raised many concerns and opportunities.

Read More

Jun 28, 2023

Top 9 Reasons to Invest in a Mobile App for Your RestaurantGood restaurants are needed everywhere, similarly, those restaurants need a good mobile application. Wondering why? Let’s find out.

Read More

Jun 26, 2023

The Rise of Fantasy Apps: Exploring the Trend and Market OpportunitiesTechnology is making fantasy apps more popular than ever before, despite traditional fantasy sports' popularity.

Read More

Jun 20, 2023

Exploring Ruby on Rails Framework: Key Features and BenefitsHave you ever heard of RoR or Ruby on Rails?

Read More

Jun 19, 2023

10 Tips and Tricks to Choose the Best App Development Partner for Your BusinessA well-designed app is not easy to create today. A single app must be developed over the course of several months, and obtaining the desired app may take up to ten months.

Read More

Jun 15, 2023

How to Build an Instant Grocery Delivery App: A Guide for Business OwnersHow many of you have thought at least once about fulfilling our grocery needs in the comfort of our homes? Almost everyone, right?! We are in an era where almost everything can be delivered to your doorstep within no time, and grocery apps are not left behind in the lane as well.

Read More

Jun 14, 2023

Performance Optimization Techniques in React Native TechnologyReact Native is without a doubt the method of choice for developing hybrid apps in the future. It provides high performance, adaptability, scalability, speed, and agility.

Read More

Jun 12, 2023

How to Integrate Front-End Frameworks with Ruby on RailsDo you know building solid and dynamic web apps with Ruby on Rails (RoR) and front-end framework integration may be quite effective?

Read More

Jun 08, 2023

A Guide To Hiring Full-Stack Developers For Web ApplicationsInstead of making several purchases, we always look for a package, whether it's making hotel reservations, dining out, or hiring a developer.

Read More

Jun 07, 2023

Everything You Should Know About Web App Development's Impact on Your BusinessThere’s a reason why the IT sector is at its peak and the reason is surging web app development. The digital world generates a huge demand for different websites and applications, aiding in revenue generation for businesses.

Read More

Jun 06, 2023

How Blockchain Boosts Healthcare? Trends,Innovations & Advantages!In recent years, blockchain technology has emerged as a game-changer in various industries, and one area where its potential impact is gaining significant attention is healthcare. The decentralized and secure nature of blockchain holds immense promise for transforming the healthcare paradigm.

Read More

Jun 05, 2023

How to build a RESTful APIs: Power Up Your Development with Ruby on RailsFirst of all, APIs. What are they?

Read More

Jun 01, 2023

Top 15 Best Database For Web Application Development to Use in 2023Now imagine you have created a website, but do you have proper data and record about how many users are coming to your website and what pages they have visited?

Read More

May 29, 2023

5 Ways An LMS Can Revolutionize Your Organization's Training ProgramsLearning has come a long way from the days of writing every sentence on paper or keeping hundreds of notebooks.

Read More

May 24, 2023

How to Choose the Right Learning Management System for Your OrganizationThere was a time when e-learning was an imaginary concept but it turned into reality a long ago, and COVID-19 restrictions have fueled this industry. All this became possible with the learning management system or simply LMS.

Read More

May 23, 2023

5 Ways a Learning Management System (LMS) Can Revolutionize Your Organization's Training ProgramsDo you concur that failing to adjust to change can sometimes result in a significant loss?

Read More

May 22, 2023

The Impact Of ChatGPT On Social MediaDo you know which is the most AI-Powered tool currently in the market?

Read More

May 16, 2023

The Future of Learning Management Systems: Trends and Predictions for 2023 and BeyondNo one believed earlier when someone said ‘Learning can be fun’! However, technological advancements have made the statement possible. There are several methods coming day by day to promote an interactive learning option in order to make the process enjoyable.

Read More

May 15, 2023

How is AI Transforming the Future of the Logistics Industry? (Benefits and Use Cases)AI has taken the world by storm in the last few years, and it is only going to continue at an even better pace. Since so many industries are revolutionizing with artificial intelligence, logistics is also not left behind.

Read More

May 11, 2023

Taxi Booking Mobile App Development Cost & FeaturesAre you still sending your family members to bring a taxi (Old traditions are good to have but don’t you think change is the new normal)? If yes, then you should stop! Local taxi owners charge a hefty amount of money for going to places that can be reached at half of that price.

Read More

May 10, 2023

How To Develop A Matrimonial Mobile App? A Complete Guide (Features, Process & Cost)One of the most crucial aspect of everyone's life is marriage. However, it can be difficult these days to find the right partner.

Read More

May 08, 2023

How AI Is Transforming The Healthcare Industry?Does Artificial intelligence have the potential to transform the healthcare industry?

Read More

May 05, 2023

Main Reasons Why UI/UX is the Final Stage for Widespread Web3 AdoptionDo you know that implementing the write strategy with UI/UX design can lead to mass adoption of Web3 platforms?

Read More

May 02, 2023

How AI Is Transforming The Future Of EdTech Industry?Integration of AI and machine learning is taking the world to the next level and the education sector did not remain untouched from this.

Read More

May 01, 2023

How to get investors for your mobile app startup?Are you a new startup trying to find out ways to grow your business? Or are you looking for ways to grow your existing mobile app business?

Read More

Apr 29, 2023

How to Make an On-Demand Medicine Delivery App Like 1mg?A healthy body is our most precious possession. The pandemic made us realize the value of a healthier body and more importantly, immunity. It is sad to convey that there was a time in life when almost each and every person relied on medicines.

Read More

Apr 26, 2023

How to Develop a Fantasy Sports Mobile App like Dream11?Who doesn’t like sports?

Read More

Apr 25, 2023

Advantages of Utilizing Ruby on Rails for Application Development in 2023The fast-paced environment waits for no one, and Ruby on Rails (RoR), understood the assignment better than any other framework. Productive frameworks like Ruby have transformed the way of working in the web development culture all over the world.

Read More

Apr 24, 2023

How to create a mobile app like UnacademyThinking to build a mobile app like Unacademy?

Read More

Apr 17, 2023

Top 8 Reasons Why Your E-Commerce Business Needs a Mobile AppWant to scale up your eCommerce business revenue?

Read More

Apr 13, 2023

How To Build A Telemedicine App in 2023? (A-Z Guide)Have you heard of the term "Telemedicine"?

Read More

Apr 12, 2023

How to Create the Wireframe of Your Application in 2023Are you wondering how wireframes can help your application stand out?

Read More

Apr 06, 2023

10 Tips to Create a Modern App UI/UX Design for Your BusinessThere are a lot of modern applications, so what makes some of them unique in the market?

Read More

Apr 05, 2023

Why use Ruby on Rails for your product development in 2023A wide variety of frameworks are available on the market. However, Ruby on Rails web application development is the most popular and preferred by many developers and firms.

Read More

Apr 04, 2023

How to Develop an Agritech Mobile App?Digital technology is transforming agriculture and food production on a global level.

Read More

Mar 28, 2023

Why Do USA Clients Prefer to Outsource Projects to IndiaAre you planning to outsource your next project to India?

Read More

Mar 28, 2023

10 UX/UI Design Trends to Watch for in 2023UI/UX design is a creative field that requires a unique approach every time you create something new. It also helps businesses in

Read More

Mar 27, 2023

Top 8 Benefits of ReactJS For Your Application DevelopmentThe new digital world can’t live without mobile and web applications

Read More

Jan 20, 2023

10 Game-Changing Web Development Trends of 2025 Every CTO Must KnowThere are around 1.14 billion websites in existence right now. The market for web development is expanding quickly, and in this cutthroat competition, those who stay on top of the trends succeed.

Read More

Jan 17, 2023

Why You Should Hire A Dedicated Remote Developer In 2023Since working remotely is becoming more common, people are often doing it these days. Employers can save money by recruiting remote workers since there are fewer overhead costs and lower employee turnover.

Read More

Jan 11, 2023

How To Find The Right MVP Developer For Your Startup IdeaAre you a startup trying to figure out how to maximize the potential of a minimum viable product (MVP)?

Read More

Dec 28, 2022

How Technology Is Transforming The Logistics Business?Online shopping trends have accelerated eCommerce growth in recent years, which has stimulated the growth of logistics services to optimize the supply chain management system.

Read More

Dec 22, 2022

Healthcare Mobile App Revenue Tips - 8 Ways To Grow Your BusinessAre you trying to find ways for your mobile healthcare app to make money but having trouble doing so?

Read More

Dec 16, 2022

Impact Of Technology And Automation On EducationAutomation is challenging, but what comes with hardships always pays off. Any industry loss is always attributed to unending demands and resource scarcity.

Read More

Nov 10, 2022

Top Mobile App Ideas For Restaurant And Food Industry 2022-23Globally, the food industry is rapidly expanding. From USD 111.32 billion in 2020, it is anticipated to increase to USD 154.34 billion in 2023. Inevitably, mobile apps are now a part of life in the food industry.

Read More

Sep 01, 2022

How Agile Technology Benefits Software Development?"Still, stuck at why to use agile methodologies? We are here to assist you in your search. "

Read More

Aug 03, 2022

Top React Developer Tools For Mobile App DevelopmentImproving performance can be tedious for a React Developer, but what makes it achievable are the right tools they choose.

Read More

Aug 03, 2022

Hire Remote Developers!Dedicated resource hiring is preferred by a majority of organizations that intend to put a professional IT team in place for building a website, mobile application, or customized software.

Read More

Jul 13, 2022

Key Reasons To Outsource Web DevelopmentTime is money and who better than a smart business person can understand this? If you also run a business and want to save time, this blog is for you.

Read More

Jul 08, 2022

Advantages Of Hiring A Global Staffing Agency For Your Start-UpThe struggle of hiring a perfect candidate for the job is very well-known for a business owner. But have you ever wondered how easy this process can get if you consider taking help from a global staffing agency?

Read More

Jul 05, 2022

Most Preferred Framework For Mobile App Development 2024It’s no surprise that mobile apps have become an integral part of everyone’s lives. Whether you want to choose a good spot for an outing or a book to read, taking the smartphone out of your pocket remains constant, because you have apps for everything.

Read More

Jul 01, 2022

An In-Depth Guide to Content Management System (CMS)Implementing a Content Management System (CMS) can empower your business website. It can be a game-changing investment decision to godspeed up your digital journey.

Read More

Jun 28, 2022

The Ultimate Guide To Mobile Application Development 2024The ever-rising demand for custom software development has revolutionized modern-day businesses with tremendous access to information

Read More

Jun 27, 2022

Microservices The Shining Star Of New Age IT InfrastructureChanging design patterns and race to substantiate the modern design and delivery approach Microservices architecture has been the face of the shift and has been a potential front runner in mainstream design process and methodology

Read More

Jun 21, 2022

Multi Tenant Architecture!As per a report by Gartner, by the end of 2022, the cloud services industry is expected to grow exponentially by 40%, and the market size of the cloud services industry will be approximately 3X the overall growth of IT services.

Read More

Jun 10, 2022

Trending UI/UX DesignThe business value of design aesthetics is no more a question to be asked. In this era of digital transformation, user experience is what drives a software product’s success, whether B2B or B2C. Hence, it has become critical for businesses to understand the significance of seamless and unique UI/UX design services for their product.

Read MoreTurn Your Billion-Dollar Dating App Idea Into Reality!

- Contact Us

Contact Us

Contact Us

As global industries shift toward digitization, the need for secure, efficient, and transparent systems becomes more urgent. Blockchain, often misunderstood as just the foundation of cryptocurrencies, is rapidly proving itself as a transformative force in enterprise technology.

Blockchain development is not about jumping on a trend—it's about building infrastructure that can handle the demands of modern business ecosystems. For organizations looking to improve data integrity, reduce friction in transactions, and eliminate unnecessary intermediaries, blockchain has become more than relevant. It’s foundational.

What Is Blockchain Development?

In a blockchain, data is recorded and maintained across a distributed network, eliminating the need for a central authority. This ledger is made up of "blocks" that contain information and are connected together with cryptographic procedures. Once recorded, data remains tamper-proof and unalterable without consensus from the network, ensuring both immutability and reliability.

Blockchain development involves creating applications and systems that leverage blockchain architecture to solve real-world problems. These may include automating contract execution, tracking digital assets, sharing verifiable data across stakeholders, or removing the need for centralized control in sensitive systems.

It combines backend logic, smart contract deployment, protocol integration, and front-end user experience—all while adhering to the principles of decentralization, transparency, and security.

Why Blockchain Is Crucial for Business

The power of blockchain lies in its ability to solve key issues that traditional systems cannot address efficiently:

- Decentralized trust: Removes the requirement for third-party verification.

- Permanent audit trails: Enhances compliance and data verification.

- Frictionless automation: Smart contracts enable real-time, rule-based automation.

- Shared truth: All parties operate from a single source of verified data.

Organizations that implement blockchain are not only streamlining operations—they're creating new business models that were previously not viable due to technical limitations or trust concerns.

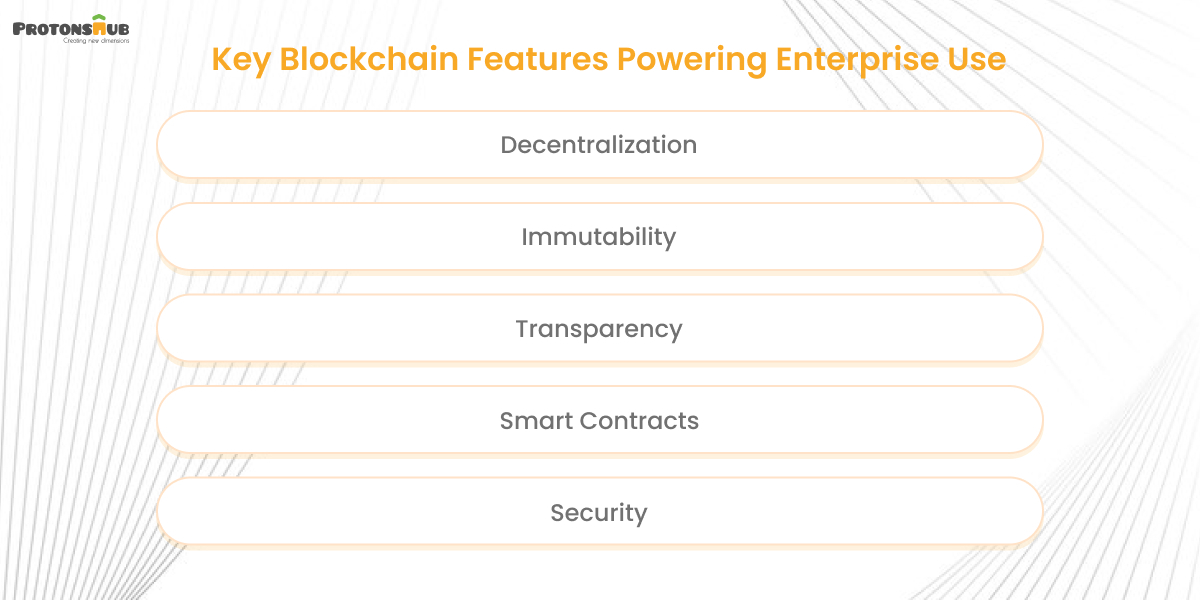

Core Features That Drive Enterprise Adoption

Blockchain’s increasing relevance in business technology is not accidental—it stems from a set of foundational features that directly address the limitations of traditional systems. From data security and system reliability to process automation and transparency, blockchain offers a redesigned approach to building digital infrastructure for enterprises.

Here’s a closer look at the core features that make blockchain so attractive to modern businesses:

1. Decentralization

Blockchain’s decentralized architecture stands out as one of its most innovative features.Traditional business systems typically rely on a central authority—whether it’s a bank, administrator, or cloud provider—to validate, store, and manage data. This creates a single point of failure and often leads to bottlenecks, inefficiencies, and security vulnerabilities.

Blockchain eliminates this dependency by distributing data and decision-making power across a peer-to-peer network. Each participant (or node) holds a copy of the ledger and contributes to consensus, removing the risk associated with centralized control.

Why It Matters for Enterprises:

- Increased Resilience: System downtime or corruption at a single point does not compromise the entire network.

- Data Sovereignty: Stakeholders can independently verify transactions without relying on third parties.

- Collaborative Infrastructure: Ideal for consortiums or multi-party workflows where trust needs to be shared but not centralized.

2. Immutability

Immutability refers to the unchangeable nature of data stored on a blockchain. Once a transaction is added to the ledger, it is cryptographically linked to the previous record and cannot be changed or removed without affecting all subsequent blocks, which is computationally unfeasible in genuine networks.

This feature is essential for industries where data integrity is paramount, such as financial services, healthcare, legal systems, and public record management

Why It Matters for Enterprises:

- Audit Trails: Provides verifiable histories of transactions or actions, which is especially useful in compliance-heavy sectors.

- Accountability: Reduces fraud, manipulation, and data tampering risks.

- Legal Validity: Immutable records hold higher evidentiary value in disputes or regulatory scrutiny.

3. Transparency

Blockchain operates on a shared, distributed ledger where every authorized participant can access the same set of verified data. This level of transparency is unprecedented in traditional systems, where different departments or companies may maintain siloed databases with conflicting versions of the truth.

In public blockchains, every transaction are visible to everyone. In private or consortium blockchains, transparency is permissioned but still consistent across stakeholders.

Why It Matters for Enterprises:

- Trust Building: Transparent data sharing reduces friction between business partners and consumers.

- Real-Time Auditing: Regulators or compliance teams can access real-time, read-only views of transactions.

- Operational Efficiency: Less need for reconciliations and error correction between departments or parties.

4. Smart Contracts

Smart contracts are digital agreements that execute automatically and are maintained on the blockchain. They automatically carry out actions—like processing payments, sending notifications, or releasing documents—once specific conditions are fulfilled. Built to be tamper-proof and transparent, these contracts operate without the need for human intervention, ensuring trust and reliability.

Unlike traditional software scripts, smart contracts operate in decentralized environments and are visible to all relevant participants, ensuring transparency and trust.

Why It Matters for Enterprises:

- Automation: Eliminates manual approvals, middlemen, and paper-based processing.

- Speed & Accuracy: Transactions are executed instantly when conditions are met.

- Cost Reduction: Reduces overhead costs tied to operations, compliance, and legal enforcement.

5. Security

Blockchain architecture is built for high-grade security. It uses advanced cryptographic techniques like hashing, digital signatures, and public/private key encryption to authenticate transactions and participants. The decentralized nature of the network also makes it extremely resistant to tampering, as any attack would require simultaneous compromise of a majority of nodes.

Furthermore, the consensus mechanisms used (such as Proof of Stake, Proof of Work, or BFT) provide additional layers of protection by validating only legitimate transactions.

Why It Matters for Enterprises:

- Cyberattack Resistance: No central server means no easy target for hackers.

- Data Integrity: Cryptographic verification ensures only authorized users can initiate or approve changes.

- Privacy with Control: Enterprises can implement permissioned blockchain networks with strict access rules.

[Also Read: Blockchain Development Guide: Everything You Need to Know]

How Blockchain Development Works

Developing blockchain solutions involves a multi-layered approach that blends decentralized architecture with secure protocols, seamless integration, and intuitive user experience.

Platform Selection

Choosing between public (e.g., Ethereum, Solana), private (e.g., Hyperledger Fabric), or consortium blockchains depends on your use case—considering factors like data sensitivity, access control, scalability, and regulatory requirements.

Consensus Mechanisms

The consensus mechanism determines how a blockchain network validates and agrees on the state of transactions. Common types include:

- Proof of Work (PoW) – Highly secure but resource-intensive.

- Proof of Stake (PoS) – More energy-efficient and scalable.

- Byzantine Fault Tolerance (BFT) – Common in permissioned blockchains.

Smart Contract Development

Smart contracts—automated scripts that execute business logic—are developed using blockchain-specific programming languages:

-

Solidity – Widely used for Ethereum-based applications.

-

Rust or C++ – Preferred for high-performance blockchains like Solana.

-

Go/Java – Common for enterprise frameworks like Hyperledger.

System Integration

To deliver real business value, blockchain must seamlessly integrate with existing enterprise systems such as ERPs, CRMs, and cloud platforms—enabled through APIs and SDKs that ensure interoperability.

User Experience (UX)

For mass adoption, decentralized apps (DApps) must offer user-friendly interfaces while handling blockchain-specific actions such as wallet authentication, gas fee estimation, and transaction confirmation.

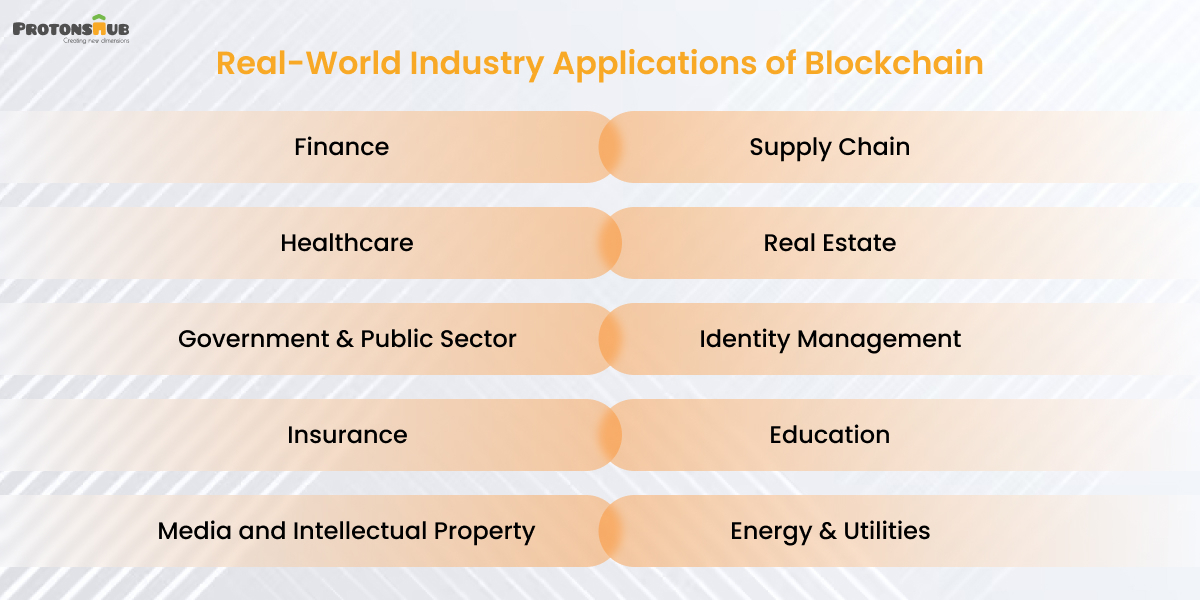

Real-World Use Cases Across Industries

Across various industries, blockchain is driving innovation by solving long-standing challenges and unlocking new efficiencies. Here are the industries where blockchain is making a significant impact through real-world use cases:

Finance

Blockchain reduces the time and cost of cross-border transactions, automates settlements, and provides secure asset tokenization. It supports decentralized finance (DeFi) systems that work without intermediaries.

Use Case: Settlement times reduced from three days to seconds in cross-border banking via Ripple or Stellar-based platforms.

[Also Read: How Blockchain Technology Can Revolutionize the Fintech Industry]

Supply Chain

Enables end-to-end traceability, real-time inventory tracking, and anti-counterfeit verification. Every entity in the chain—from producer to retailer—shares a tamper-proof record.

Use Case: Major retailers use blockchain to trace food items from farm to shelf, identifying contamination sources in minutes.

Healthcare

Secures patient records, streamlines claims processing, and ensures medical data privacy while enabling interoperability across providers.

Use Case: Blockchain platforms give patients control over their own health data, enabling selective access to healthcare providers.

Real Estate

Eliminates redundant paperwork, simplifies title verification, and enables smart contracts for faster property transactions.

Use Case: Blockchain-based digital deed systems reduce fraud and speed up ownership transfer.

Government & Public Sector

Facilitates transparent voting systems, digitized land records, and efficient public benefits management.

Use Case: Pilot e-voting systems on blockchain ensure election integrity with verifiable participation.

Identity Management

Empowers individuals with control over their digital identities through Decentralized Identity (DID) systems.

Use Case: KYC processes become faster and safer by verifying users through blockchain-based identity proofs.

Insurance

Automates claims processing, minimizes fraud, and improves customer experience through rule-based smart contracts.

Use Case: Blockchain-powered insurance contracts can automatically trigger payouts based on real-time weather conditions or event data.

Education

Secures academic credentials and makes them instantly verifiable across institutions and employers.

Use Case: Blockchain-issued degrees reduce falsification and speed up background verification.

Media and Intellectual Property

Monitors ownership, usage, and royalties in real time to safeguard creators' rights and ensure transparent, fair compensation.

Use Case: Musicians receive royalty payments instantly when their songs are streamed, via smart contracts.

Energy & Utilities

Supports peer-to-peer energy trading and tracks carbon credits to ensure sustainability goals are met.

Use Case: Smart meters record and trade excess solar energy between households on a blockchain platform.

Common Implementation Challenges in Blockchain Development

While blockchain technology offers transformative potential, its implementation is not without challenges. For many businesses, the road to effective blockchain integration is filled with technical, strategic, and regulatory hurdles. Understanding these obstacles is critical for organizations looking to harness blockchain's advantages without missteps.

Below are the most common challenges companies face when adopting blockchain technology—and what they mean for real-world implementation.

1. Choosing the Right Blockchain Platform

One of the earliest and most crucial decisions is selecting the appropriate blockchain network. Public blockchains such as Ethereum ensure transparency and decentralization, but they often trade off speed and privacy. Private or permissioned blockchains, such as Hyperledger Fabric or Corda, allow better control but reduce decentralization.

The Challenge:

Selecting a platform that balances security, scalability, privacy, and performance is complex—especially for businesses unfamiliar with the technical trade-offs.

Consideration:

Businesses need expert consultation to align platform capabilities with business goals. Misaligned platform choice can cause costly redesigns later.

2. Integration with Existing Systems

Most businesses already have legacy systems like ERPs, CRMs, or internal databases. Blockchain needs to work alongside these systems without causing disruption.

The Challenge:

Blockchain is built on decentralized, cryptographic foundations, while traditional systems depend on centralized authority. Bridging the two can create architectural complexity and performance issues.

Consideration:

Integration should be approached with middleware solutions, APIs, and a modular architecture that supports interoperability.

3. Lack of Skilled Talent

Blockchain development requires specialized skills—smart contract development, cryptographic security, distributed system design, and protocol engineering. These are not commonly found in traditional IT teams.

The Challenge:

Hiring skilled blockchain developers is both costly and highly competitive. A lack of expertise can result in security vulnerabilities, project delays, or a poor user experience.

Consideration

During the initial stages, many businesses choose to collaborate with blockchain development companies or bring in external experts to strengthen their team

4. Regulatory Uncertainty

Blockchain regulations vary widely across regions and are still evolving. Businesses working in finance, healthcare, or data-sensitive industries must navigate legal grey areas around data privacy, crypto tokens, and smart contract enforcement.

The Challenge:

Laws governing cryptocurrencies, data storage, cross-border transfers, and tokenized assets differ drastically from country to country. Failure to act or misinterpret regulations can result in serious compliance challenges.

Consideration:

Projects must include legal consultation from the start and adopt flexible architectures that can evolve with regulation.

5. Scalability Constraints

Public blockchains typically face challenges with transaction throughput. Ethereum, for example, has dealt with network slowdowns and increased gas fees during high-demand periods.

6. Security Risks

While the blockchain protocol itself is generally secure, the applications built on top—particularly smart contracts—can be vulnerable to bugs or exploits.

The Challenge:

Code immutability means that once a smart contract is deployed, bugs can’t be fixed without significant network coordination. Security breaches can lead to major losses of funds or sensitive data.

Consideration:

Rigorous smart contract audits, test-driven development, and formal verification methods are essential before deployment.

7. User Experience (UX) Complexity

Interacting with blockchain-based applications often involves wallet setups, managing cryptographic keys, and understanding transaction fees (gas). For the average user, this can be confusing and frustrating.

The Challenge:

If users don’t understand how to engage with a blockchain platform, adoption stalls—even if the technology behind it is robust.

Consideration:

Designing intuitive, user-friendly front ends and offering custodial wallet options or abstracted blockchain mechanics can improve adoption rates.

8. Data Privacy vs. Transparency

One of blockchain’s most praised features—data transparency—can become a liability in industries where confidentiality is critical, such as healthcare, insurance, or government.

The Challenge:

How do you maintain transparency for verification while keeping sensitive data private?

Consideration:

Techniques like zero-knowledge proofs, encryption, private chains, or off-chain storage should be used to strike the right balance.

9. High Initial Costs and ROI Uncertainty

Implementing blockchain involves not just development, but also planning, compliance, testing, infrastructure, and post-deployment support.

The Challenge:

Many companies hesitate to invest due to unclear ROI or long-term value. The benefits of blockchain are often long-term and strategic rather than immediate.

Consideration:

Starting with a Minimum Viable Product (MVP) and defining KPIs aligned to business outcomes can help prove value early.

10. Governance and Change Management

Who controls the blockchain? Who updates smart contracts? How are disputes resolved in a decentralized network?

The Challenge:

Blockchain eliminates central authority, but also removes the ability to quickly fix errors, reverse transactions, or manage upgrades centrally.

Consideration:

Governance frameworks, multisig protocols, and DAO models can provide structured decision-making and control.

How Protonshub Technologies Can Help You

Blockchain development is not just a technical trend—it’s a strategic transformation in how businesses build trust, share data, and automate operations. As industries face growing demands in security, compliance, and efficiency, blockchain offers a modern foundation for digital infrastructure.

Protonshub Technologies helps organizations turn this promise into practical impact. Whether you’re building a decentralized application (DApp), deploying smart contracts, or integrating blockchain into your legacy systems, Protonshub delivers tailored solutions that align with your business goals.

With hands-on experience in leading platforms like Ethereum, Hyperledger, Solana, and Polygon, the Protonshub team brings deep expertise in consensus models, security architecture, and user-centric design. From early-stage MVPs to full-scale enterprise systems, every solution is built to be secure, scalable, and future-ready.

For forward-thinking businesses, blockchain is more than innovation—it’s a competitive edge. With Protonshub Technologies as your partner, you gain a team that understands both the technology and its real-world application—helping you define the next generation of secure and intelligent business systems.

Frequently Asked Questions

Newsletter

Subscribe to Weekly - Get five biggest headlines in blockchain straight to your inbox

Trending Blog

Jul 03, 2024

How Blockchain Technology Can Revolutionize the Fintech Industry

Feb 16, 2024

AI in E-commerce: 8 Ways It’s Transforming the Business

Feb 13, 2024

Top Emerging Web Design Trends for 2024 and Beyond [Updated]